When selling or buying a car through a private arrangement involving financing, the entire transaction hinges on trust. However, trust alone isn't enough to protect both parties' financial interests. This is where a formal, written agreement becomes indispensable, and a high-quality Auto Promissory Note Template serves as the perfect foundation for this agreement. This legal instrument transforms a handshake deal into a legally binding contract, providing clarity and security for both the lender (often the seller) and the borrower (the buyer). It meticulously outlines the repayment terms, ensuring there is no confusion about the loan amount, interest, payment schedule, and consequences for non-payment.

A promissory note for a vehicle is far more than a simple IOU. While an IOU merely acknowledges a debt, a promissory note is a formal promise to pay that includes specific, enforceable terms. It details the "who, what, when, and how" of the loan. For the person selling the car, it acts as a legal recourse if the buyer defaults on their payments. For the buyer, it provides a clear record of their payment obligations and protects them from arbitrary changes to the loan terms. Using a structured template ensures all critical elements are included, reducing the risk of future disputes that could sour a personal relationship or lead to costly legal battles.

The versatility of this document makes it suitable for various situations beyond a typical seller-financed sale. It's an invaluable tool for formalizing a car loan between family members or friends, helping to preserve the relationship by setting clear, business-like expectations from the outset. By putting everything in writing, both parties understand their rights and responsibilities. This prevents the common pitfalls of verbal agreements, which are often subject to misinterpretation, forgotten details, and are notoriously difficult to enforce in a court of law.

This comprehensive guide will walk you through everything you need to know about using a promissory note for a vehicle sale. We will break down the essential components of a robust template, explain when and how to use one, and highlight critical legal considerations to ensure your agreement is both fair and enforceable. By the end, you'll have the confidence to structure a secure financing arrangement that protects your investment and provides peace of mind.

What is an Auto Promissory Note?

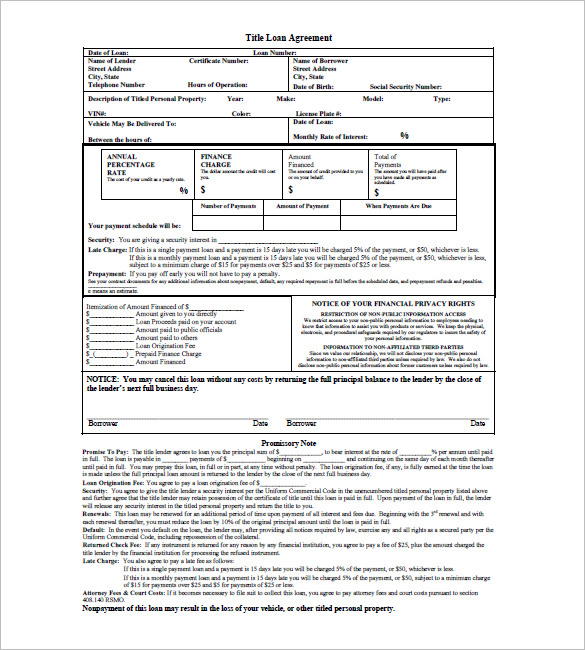

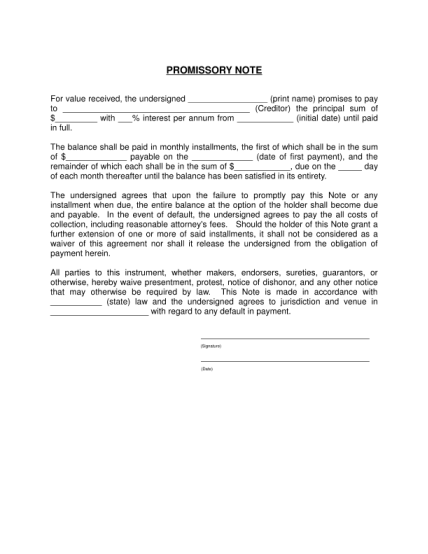

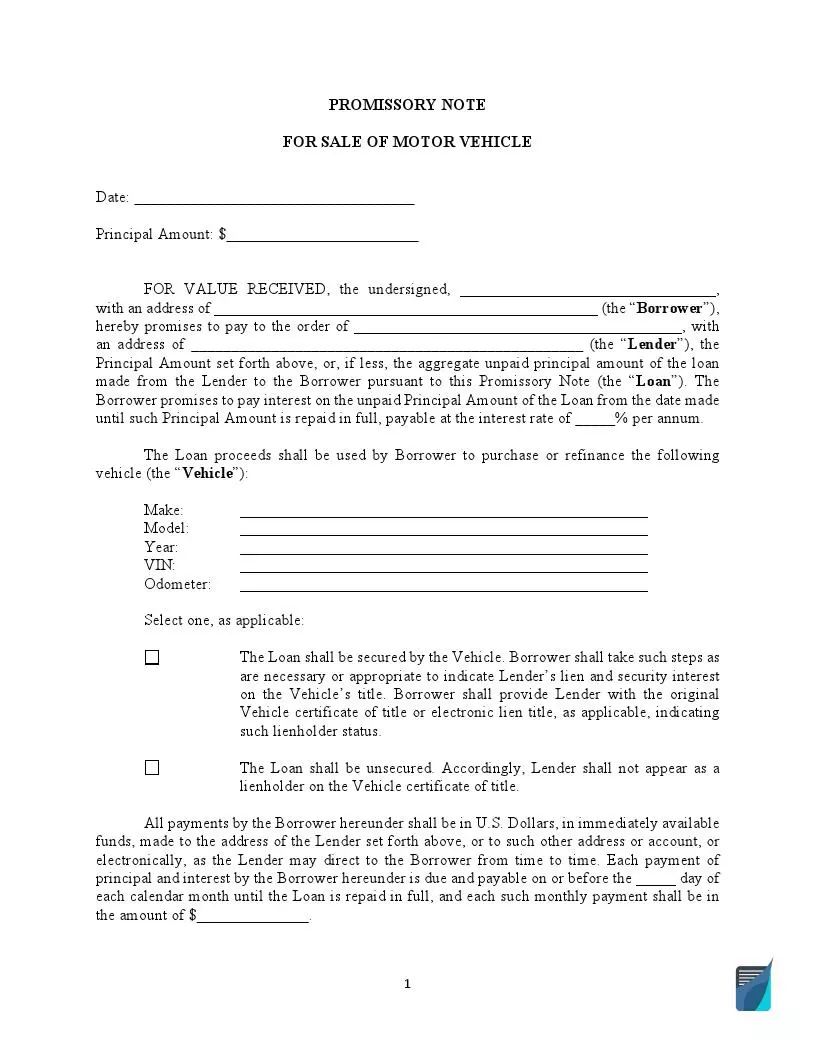

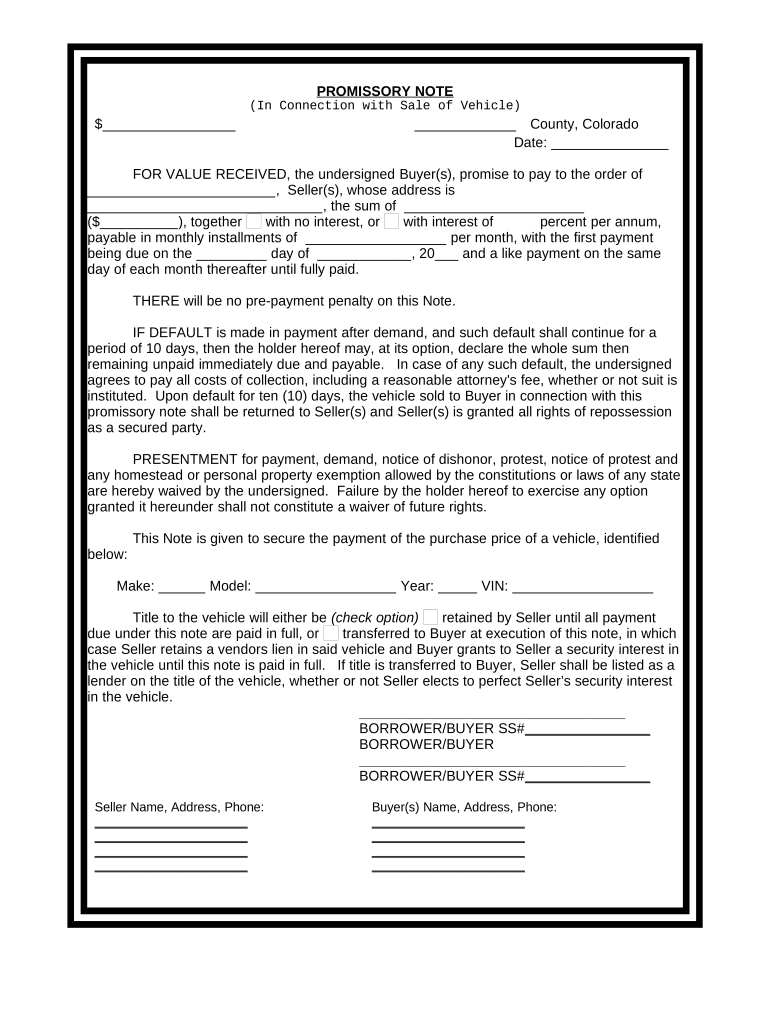

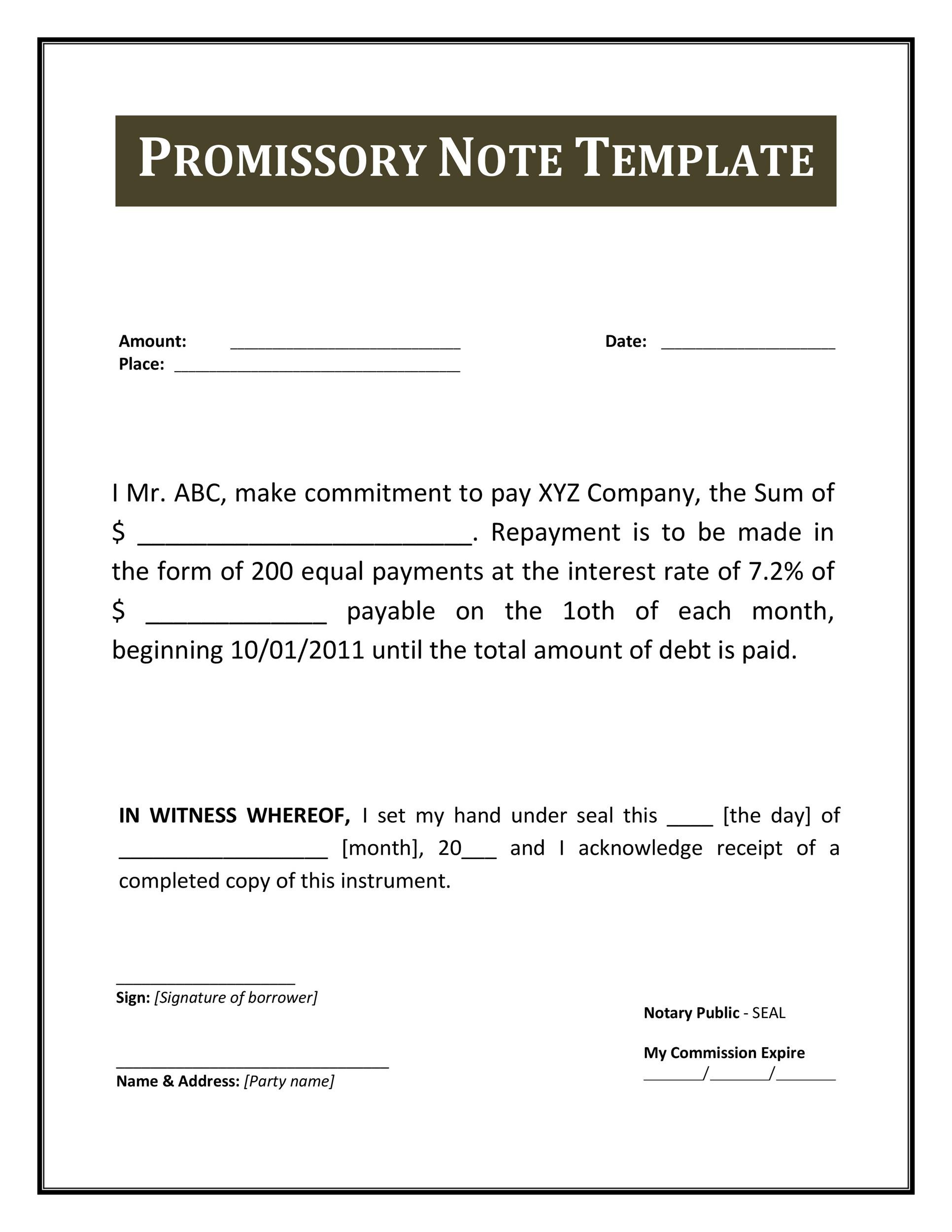

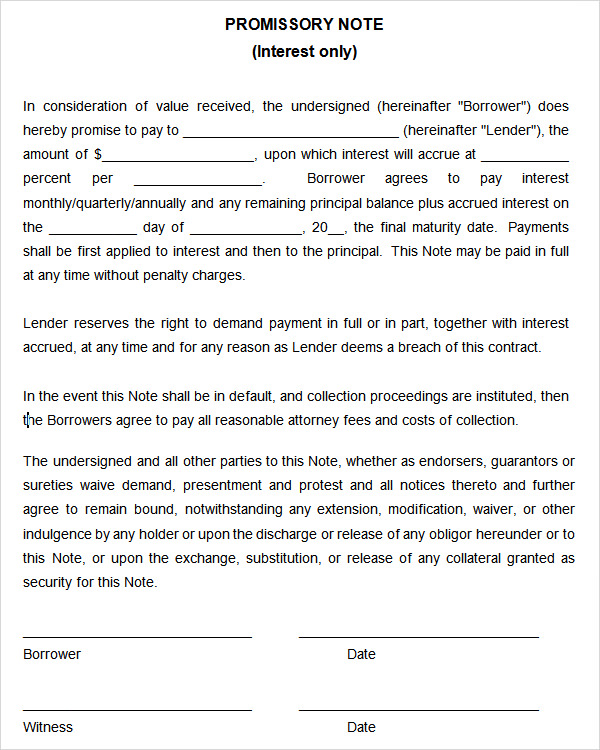

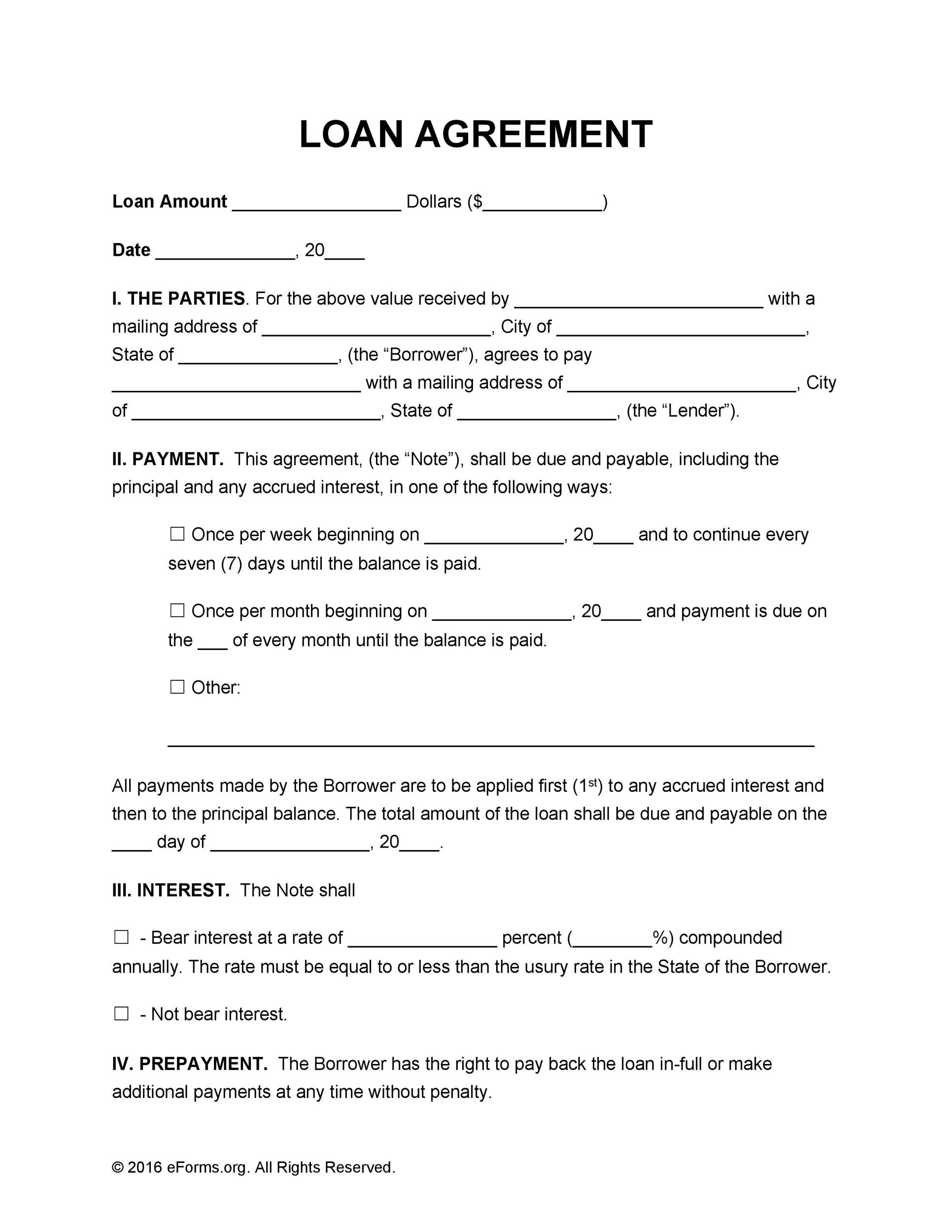

An auto promissory note is a legally binding written contract where one party (the borrower or maker) makes an unconditional promise to pay a specific sum of money to another party (the lender or payee) for the purchase of a vehicle. This document serves as the official record of the loan, detailing all the terms and conditions of the repayment plan. It's the core of any seller-financed vehicle transaction, transforming an informal arrangement into a formal, enforceable financial agreement.

The primary purpose of the note is to eliminate ambiguity. It clearly defines the loan amount (principal), the interest rate (if any), the schedule of payments, the due dates, and the penalties for late payments or default. By signing the document, the buyer legally acknowledges their debt and agrees to adhere to the repayment structure outlined within it.

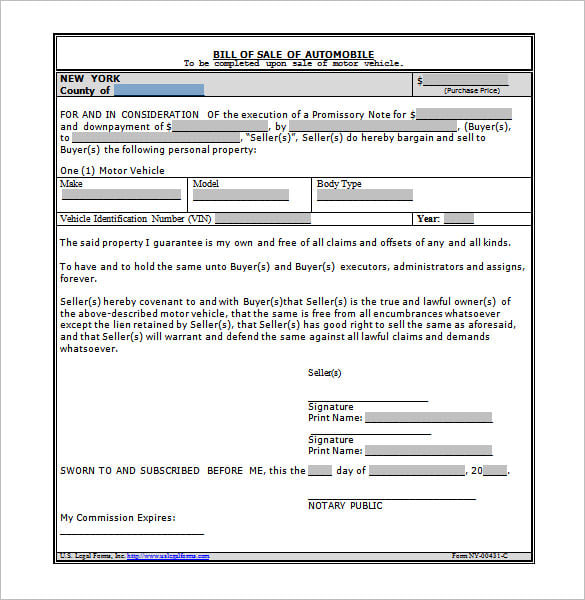

It's crucial to understand the distinction between an auto promissory note and a Bill of Sale. A Bill of Sale is the document that legally transfers ownership or title of the vehicle from the seller to the buyer. It's proof that a sale occurred. The promissory note, on the other hand, does not transfer ownership; it details the financing agreement that allows the sale to happen. The two documents work together: the Bill of Sale confirms the change of hands, while the promissory note ensures the seller gets paid according to the agreed-upon terms over time. Often, the car's title is held by the seller (lender) until the loan is fully paid, as stipulated in the note.

Key Components of a Comprehensive Auto Promissory Note Template

A generic, poorly constructed note can leave dangerous loopholes. A comprehensive template will include specific clauses that protect both parties. When you're drafting your agreement, ensure it contains the following critical components.

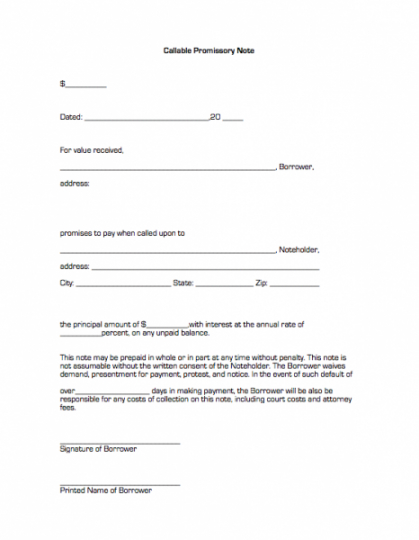

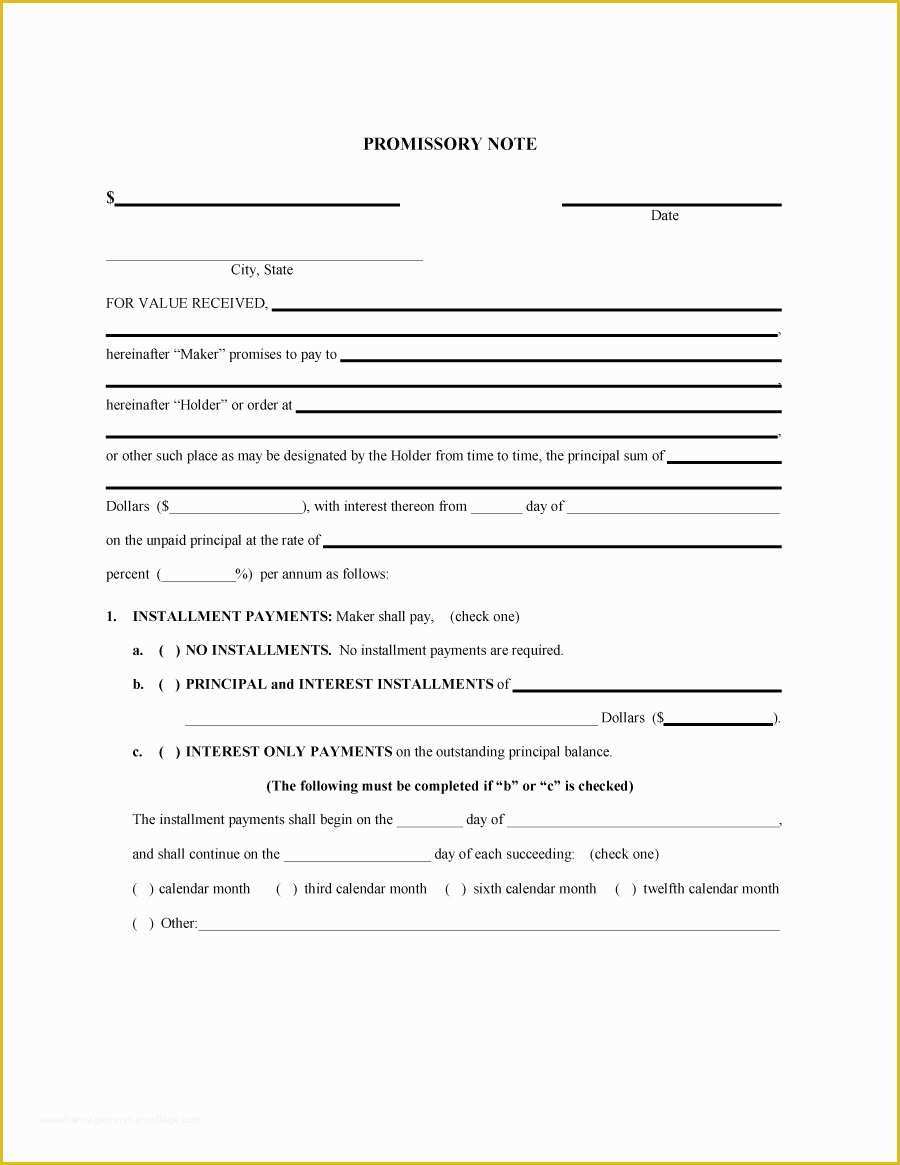

Principal Amount and Interest Rate

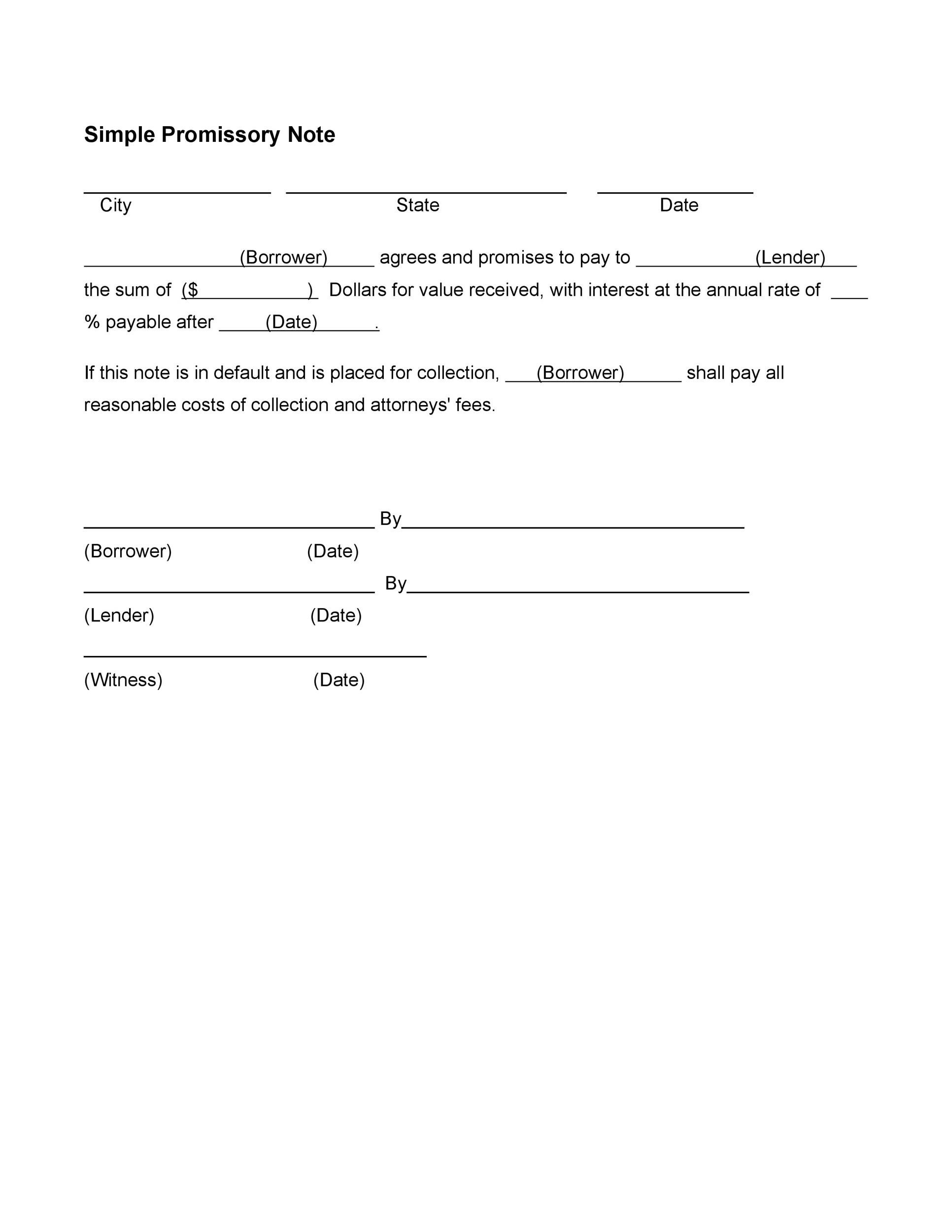

This is the financial core of the note. The principal amount is the total amount of money being loaned. For a car sale, this is typically the agreed-upon purchase price minus any down payment the buyer has made. The document must state this amount clearly in both numbers and words to avoid confusion.

The interest rate is the cost of borrowing the money, expressed as an Annual Percentage Rate (APR). If interest is being charged, the rate must be explicitly stated. It is vital to research your state's usury laws, which set a legal maximum for interest rates on private loans. Charging an illegally high interest rate can render the entire agreement unenforceable. If no interest is being charged, the note should clearly state "0% interest."

Payment Schedule

This section outlines how and when the loan will be repaid. It must be detailed and unambiguous. Key elements include:

- Payment Frequency: Specify whether payments are due weekly, bi-weekly, monthly, or on another schedule. Monthly is the most common for vehicle loans.

- Payment Amount: State the exact amount of each installment.

- Due Date: Note the specific date each payment is due (e.g., "the 1st day of each month").

- First and Last Payment Dates: Clearly list the date the first payment is due and the date the final payment is expected, which marks the end of the loan term.

- Payment Method: It's wise to specify acceptable methods of payment, such as bank transfer, certified check, or a specific online payment service, to create a clear payment record.

Late Fees and Penalties

To encourage timely payments, the note should include a clause detailing the consequences of paying late. This section should define what constitutes a "late" payment, often by including a grace period (e.g., 5-10 days after the due date). If a payment is made after this grace period, a late fee can be charged. The fee should be a reasonable, specific amount—either a flat fee (e.g., "$25 for any payment more than 5 days late") or a percentage of the monthly payment.

Default and Acceleration Clause

The note must clearly define what constitutes a default on the loan. This is typically more severe than a single late payment and might be defined as missing a certain number of consecutive payments (e.g., two or three) or being more than 30 days late on a single payment.

Crucially, this section should include an acceleration clause. This powerful clause states that if the borrower defaults on the loan, the lender has the right to demand that the entire remaining balance of the loan becomes immediately due and payable. This is a critical provision that gives the lender significant leverage to pursue legal action for the full amount owed.

Collateral Details

For an auto promissory note, the vehicle being purchased serves as collateral for the loan. This means if the borrower defaults and fails to pay the remaining balance, the lender has the right to repossess the vehicle to recover their losses. This is known as a secured promissory note.

To make this legally sound, the note must include a detailed description of the vehicle, including its:

- Make (e.g., Toyota)

- Model (e.g., Camry)

- Year of manufacture

- Vehicle Identification Number (VIN)

- Color and any other identifying features

Including the VIN is non-negotiable, as it is the unique identifier for the vehicle and is essential for any legal or repossession proceedings.

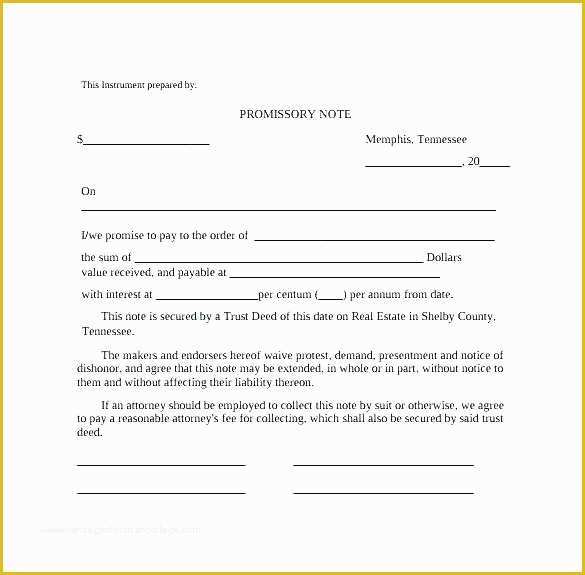

Signatures and Notarization

For the promissory note to be a legally valid contract, it must be signed and dated by all parties involved—the borrower(s) and the lender(s). The signatures indicate that all parties have read, understood, and agreed to the terms within the document.

While not always legally required in every state, having the document notarized is highly recommended. A notary public acts as an impartial witness who verifies the identity of the signers and confirms they are signing the document willingly. A notarized signature adds a significant layer of legal protection and makes it much more difficult for a party to later claim their signature was forged or that they didn't understand what they were signing.

When to Use a Promissory Note for a Car Sale

A promissory note is a flexible tool that can be used in any situation where a vehicle is sold via a private loan. The most common scenarios include:

Seller Financing: This is the primary use case. A private individual selling their car agrees to act as the bank for the buyer. Instead of the buyer getting a loan from a traditional financial institution, the seller finances the purchase and receives payments over time. This can make the car more attractive to a wider pool of buyers, but it necessitates a promissory note to protect the seller's financial stake.

Loans Between Family or Friends: Loaning money to a family member or friend to buy a car can be fraught with peril. A promissory note depersonalizes the financial aspect of the transaction and protects the relationship. It turns a casual "I'll pay you back" into a structured agreement, preventing misunderstandings about repayment expectations. It shows that both parties are taking the loan seriously.

Formalizing a Verbal Agreement: Verbal agreements are a leading cause of financial disputes. Memories fade, terms are misinterpreted, and there is no proof of the original agreement. An auto promissory note should be used to replace any handshake deal. It provides a definitive, written record that can be referenced if any disagreements arise, offering a clear path to resolution without resorting to "he said, she said" arguments.

Step-by-Step Guide: How to Create and Use Your Auto Promissory Note

Creating and implementing an auto promissory note is a straightforward process when broken down into manageable steps. Following this guide will help ensure your agreement is solid and all bases are covered.

Step 1: Find a Reliable Template

The first step is to obtain a well-drafted document. You can find a basic Auto Promissory Note Template through various online legal document providers. When selecting one, look for a template that is comprehensive and includes all the key components mentioned earlier (principal, interest, collateral, default clauses, etc.). Be cautious of overly simplistic or generic templates. It is often worth paying a small fee for a template from a reputable source that allows for customization and provides state-specific considerations.

Step 2: Fill in the Essential Details

Carefully and accurately fill in all the blank fields in the template. This information forms the legal basis of your agreement, so precision is key. Double-check every detail before proceeding:

- Party Information: Full legal names and addresses of the borrower and lender.

- Loan Details: The exact principal amount, the agreed-upon interest rate (APR), and the total loan term.

- Vehicle Information: The make, model, year, and, most importantly, the VIN of the vehicle.

- Payment Plan: The installment amount, frequency, and specific due dates.

Step 3: Negotiate and Agree on Terms

Before anyone signs, both the lender and borrower must sit down and review the completed document together. This is the time to negotiate and confirm that every term is fully understood and agreed upon. Discuss the payment schedule, the late fee policy, and the conditions of default. Transparency at this stage prevents future disputes. If any changes are made, ensure they are reflected in the final document before signing.

Step 4: Execute the Document

Executing the note means signing it. All parties must sign and date the document in the designated areas. For maximum legal protection, it is strongly recommended to sign the promissory note in the presence of a notary public. The notary will require valid identification from each signer, witness the signatures, and then apply their official stamp or seal. Notarization provides powerful, third-party verification of the signing event.

Step 5: Distribute and Store Copies

Once the document is signed and notarized, make copies. Both the lender and the borrower should retain a fully executed original or a high-quality copy for their records. Store the document in a safe and secure place where it can be easily accessed if needed, such as a fireproof safe or a secure digital cloud storage service. The lender should keep their copy for the entire duration of the loan and for a period afterward, as determined by the state's statute of limitations.

Legal Considerations and State Laws

While a promissory note is a fairly standard legal document, its enforceability can be affected by state-specific laws. Ignoring these can lead to serious legal complications.

Usury Laws: As mentioned before, every state has usury laws that cap the maximum interest rate a private lender can charge. Rates that exceed this limit are considered usurious and illegal. In some states, this could result in penalties for the lender or even void the entire loan agreement. Always verify your state's maximum APR for private loans before setting an interest rate.

Repossession Rules: The promissory note grants the lender the right to take possession of the collateral (the vehicle) in the event of a default. However, the process of repossession is strictly regulated by state law. These laws dictate how and when a vehicle can be repossessed, what notices must be provided to the borrower, and the borrower's right to redeem the vehicle. Lenders cannot simply "take the car back" without following the proper legal procedures, which may include avoiding a "breach of the peace."

Statute of Limitations: Each state has a statute of limitations for debt collection. This is the legal time limit within which a lender can file a lawsuit to collect a debt. If the borrower defaults and the lender waits too long to take legal action, they may forfeit their right to recover the money. This timeframe varies significantly by state, so it's important to be aware of the deadline in your jurisdiction.

Given these complexities, it is always a prudent choice to consult with a legal professional, especially for high-value vehicles or complex loan terms. A lawyer can review your promissory note to ensure it is compliant with all relevant state and federal laws, providing you with the highest level of protection.

Conclusion

An auto promissory note is more than just a piece of paper; it's a fundamental tool for creating a secure and transparent private vehicle financing arrangement. Whether you are a seller offering financing to attract more buyers or an individual formalizing a car loan with a friend or family member, this document is your best protection against misunderstandings, disputes, and financial loss. By transforming a verbal agreement into a clear, legally binding contract, it sets precise expectations for repayment and outlines a clear course of action if those expectations are not met.

By using a comprehensive Auto Promissory Note Template and carefully including all the essential components—from the principal and interest to collateral details and default clauses—you establish a solid legal foundation for the transaction. Remember to adhere to state-specific laws, particularly regarding interest rates and repossession, and consider having the document notarized to add an extra layer of security. Taking these steps ensures that the agreement is fair, clear, and enforceable, protecting the financial interests of both the lender and the borrower throughout the life of the loan.

0 Response to "Auto Promissory Note Template"

Posting Komentar