Creating a comprehensive and accurate personal financial statement is a crucial step towards achieving financial stability and reaching your long-term goals. Whether you're a student, a young professional, or an established individual, a well-structured financial statement provides a clear picture of your financial situation and helps you make informed decisions. This guide will walk you through creating a blank personal financial statement template, covering essential sections and offering helpful tips along the way. Blank Personal Financial Statement Template – understanding its components is the first step to taking control of your finances. It's more than just a document; it's a roadmap to a brighter financial future. Let's begin!

Understanding the Importance of a Personal Financial Statement

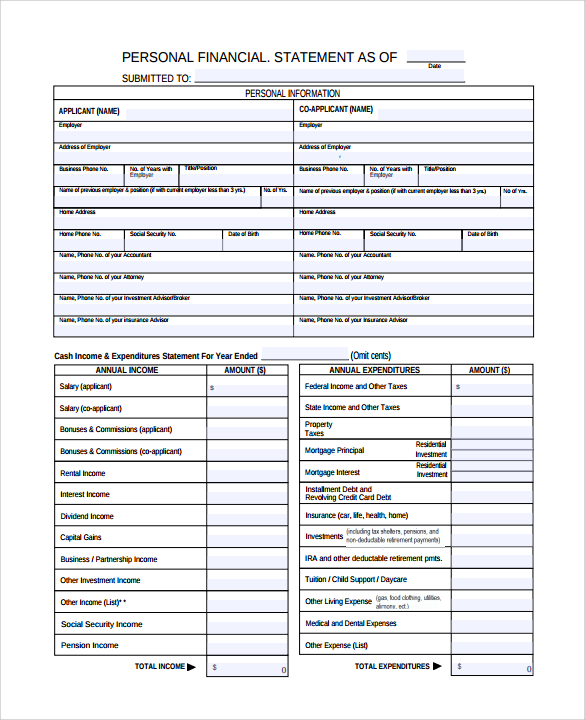

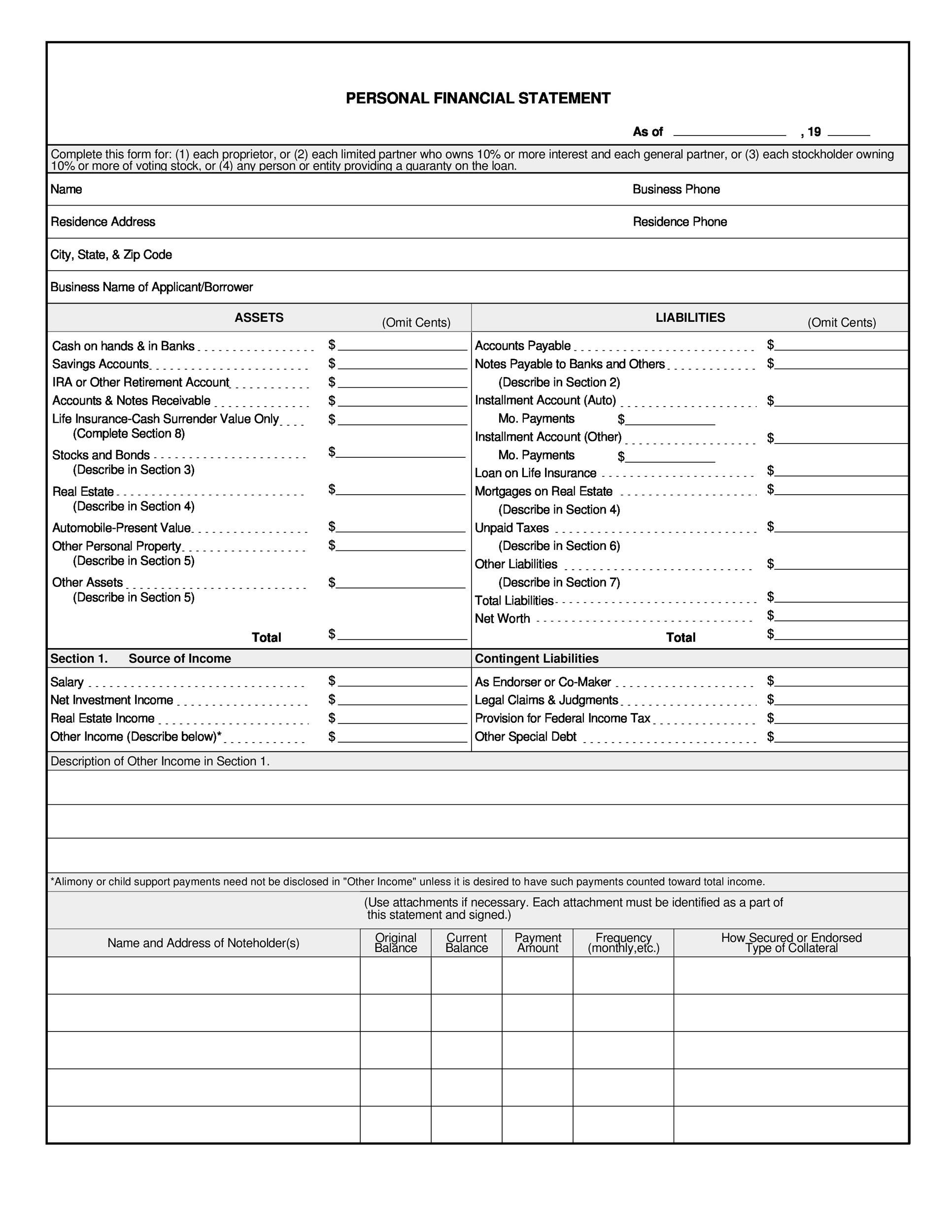

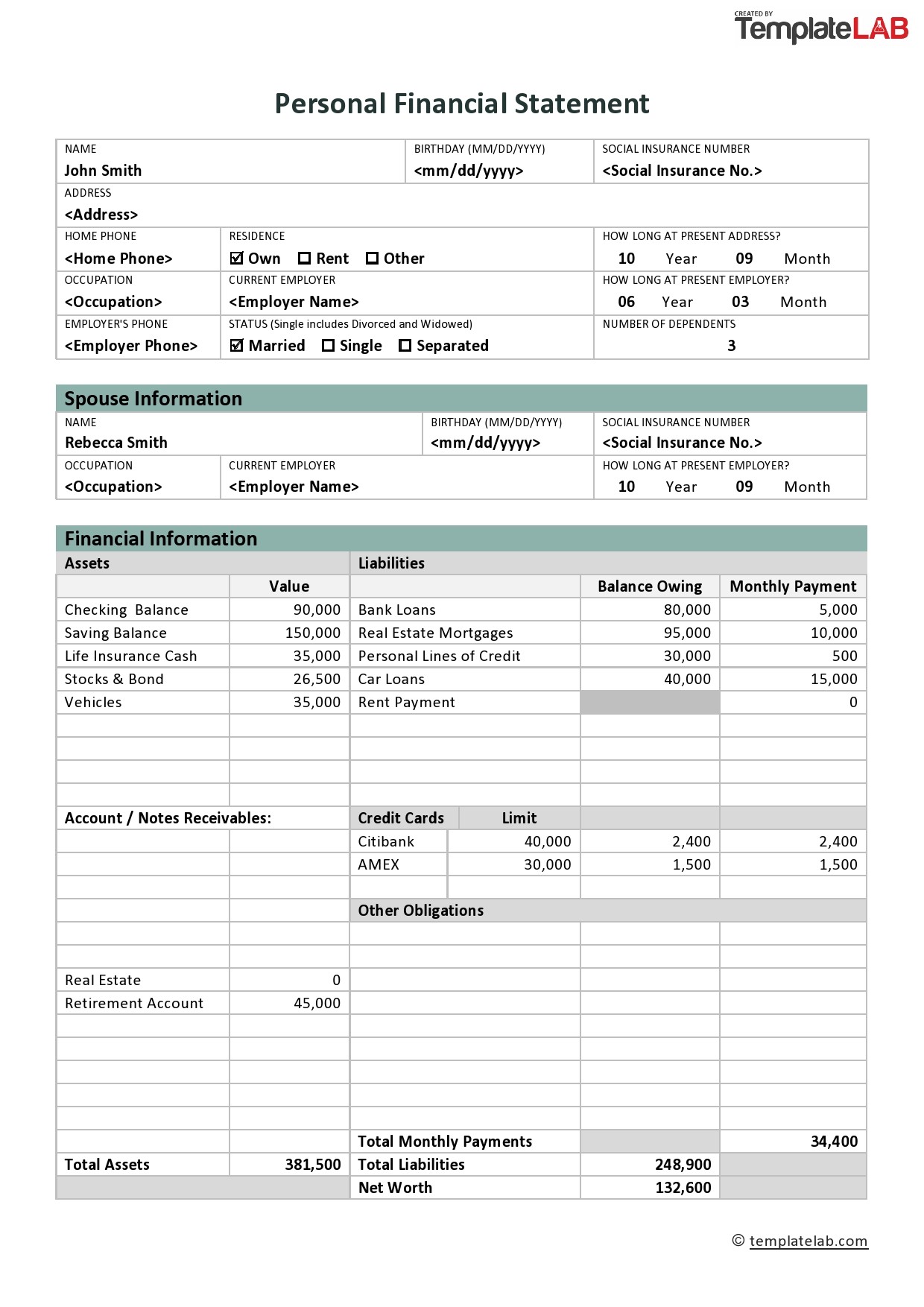

A personal financial statement is a detailed record of your income, expenses, assets, and liabilities. It's a powerful tool for tracking your progress, identifying areas for improvement, and planning for the future. It's not just for tax preparation; it's a vital tool for budgeting, saving, investing, and overall financial wellness. Without a clear understanding of your financial situation, it's difficult to make sound decisions about your money. A well-crafted statement can help you identify spending habits, pinpoint areas where you can save, and set realistic financial goals. Furthermore, it demonstrates to lenders, potential investors, and even yourself the health of your finances. The ability to accurately assess your financial standing is increasingly important in today's complex economic landscape. It's a proactive step towards securing your financial well-being.

Section 1: Income – Tracking Your Earnings

The first section of your financial statement is dedicated to documenting your income sources. Accurately tracking your income is fundamental to understanding your financial health. This includes all sources of income, both regular and irregular. It's important to categorize your income to gain a clearer picture of your overall earnings. Common income sources include:

- Salary/Wages: This is the primary source of income for most individuals. Record your salary, including any bonuses, commissions, or overtime pay.

- Freelance Income: If you work as a freelancer, track your income from each project or client.

- Investment Income: Include any dividends, interest, or capital gains from investments.

- Rental Income: If you own rental properties, accurately record your rental income and expenses.

- Side Hustles: Any additional income earned through side projects or businesses.

- Government Benefits: Include any payments you receive through programs like Social Security, unemployment, or disability.

Important Note: Keep detailed records of all income sources. Use a spreadsheet, accounting software, or a notebook to track your earnings consistently. Don't underestimate the impact of even small amounts of income. Regularly reviewing your income data will help you identify trends and adjust your budget accordingly.

Section 2: Expenses – Understanding Where Your Money Goes

The second section focuses on meticulously tracking your expenses. This is where you identify areas where you can potentially reduce spending and allocate more funds to savings and investments. Categorizing your expenses is crucial for understanding your spending patterns. Common expense categories include:

- Housing: Rent or mortgage payments, property taxes, homeowner's insurance.

- Utilities: Electricity, gas, water, trash removal.

- Transportation: Car payments, gas, insurance, maintenance, public transportation.

- Food: Groceries, dining out.

- Healthcare: Health insurance premiums, doctor visits, prescriptions.

- Debt Payments: Student loans, credit card debt, personal loans.

- Entertainment: Movies, concerts, subscriptions, hobbies.

- Personal Care: Haircuts, cosmetics, toiletries.

- Clothing: Purchases of clothing and accessories.

- Miscellaneous: Uncategorized expenses – these are important to track to identify potential areas for savings.

Tips for Tracking Expenses:

- Use a Budgeting App: Apps like Mint, YNAB (You Need a Budget), or Personal Capital can automate expense tracking.

- Categorize Everything: Be as specific as possible when categorizing expenses.

- Review Regularly: Review your expenses at least monthly to identify areas for improvement.

- Track Recurring Expenses: Pay attention to recurring expenses like rent and utilities, as these can be difficult to adjust.

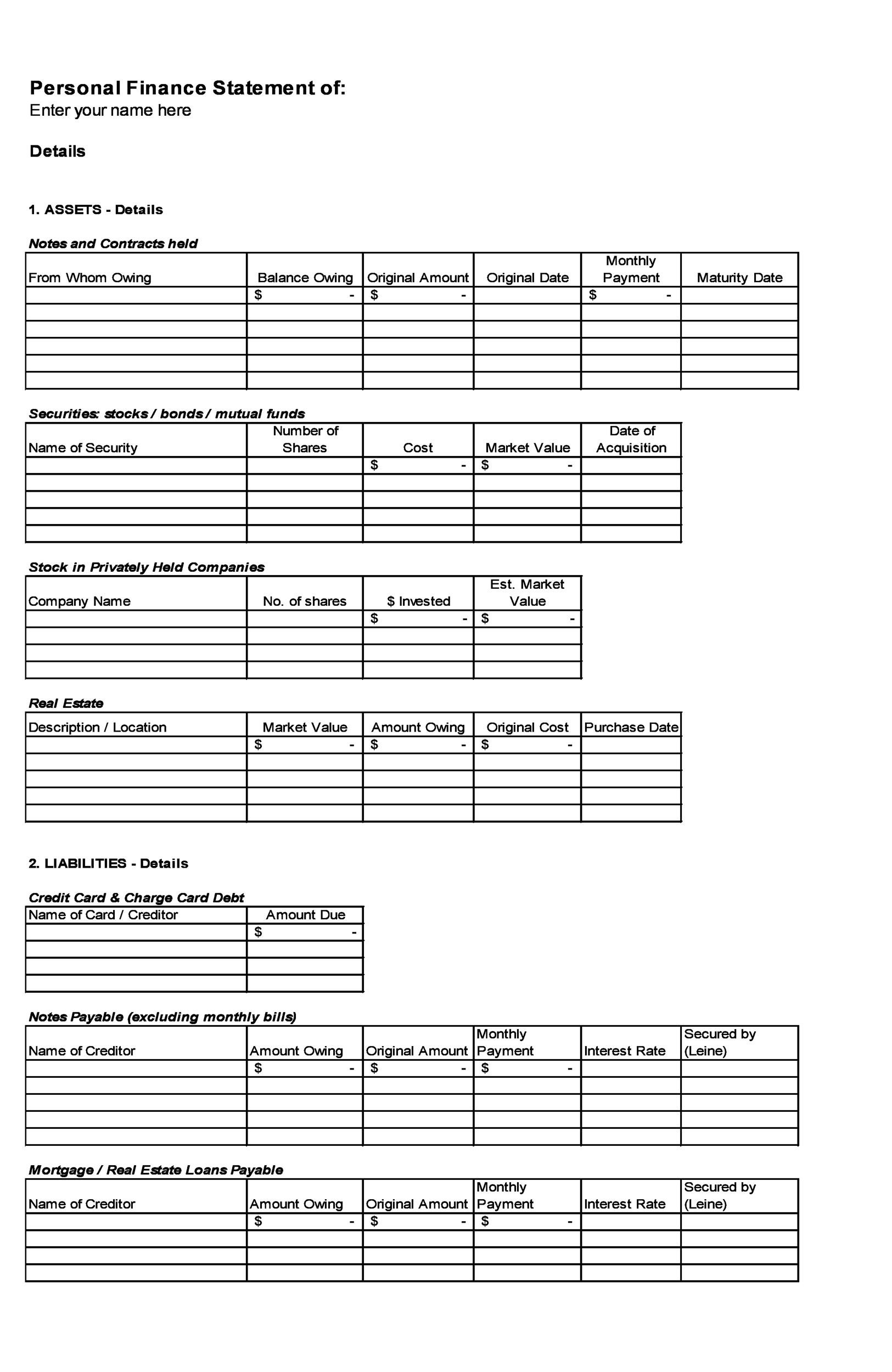

Section 3: Assets – What You Own

The assets section outlines your financial holdings. It's important to understand the value of your assets to assess your overall financial security. Assets can be categorized as:

- Cash and Savings: Checking accounts, savings accounts, money market accounts.

- Investments: Stocks, bonds, mutual funds, retirement accounts (401(k), IRA).

- Real Estate: Property, land, and other real estate investments.

- Other Assets: Vehicles, valuable collectibles, and other assets.

Important Note: Keep accurate records of the value of your assets. This information is crucial for tax purposes and for assessing your financial risk. Consider consulting with a financial advisor to determine the best investment strategy for your assets.

Section 4: Liabilities – Your Debts

The liabilities section details your outstanding debts. This includes all loans, credit card balances, and other obligations. It's important to understand the terms of your debts to avoid surprises. Common liabilities include:

- Mortgage: The loan secured by your property.

- Student Loans: Loans for education expenses.

- Credit Card Debt: Outstanding balances on credit cards.

- Auto Loans: Loans for your vehicle.

- Personal Loans: Loans for various purposes.

- Other Loans: Any other debts you have.

Tips for Managing Liabilities:

- Prioritize High-Interest Debt: Focus on paying down high-interest debt first to minimize interest charges.

- Create a Debt Repayment Plan: Develop a plan to pay off your debts over time.

- Avoid Taking on New Debt: Be mindful of your spending and avoid accumulating new debt.

Section 5: Financial Goals – Where You Want to Be

The final section of your personal financial statement is dedicated to outlining your financial goals. This is a crucial step in aligning your financial decisions with your long-term aspirations. Examples of financial goals include:

- Short-Term Goals (1-3 years): Saving for a down payment on a house, paying off credit card debt, building an emergency fund.

- Mid-Term Goals (3-10 years): Saving for a wedding, saving for a child's education, investing in a rental property.

- Long-Term Goals (10+ years): Retirement planning, funding your children's education, achieving financial independence.

How to Set Goals:

- Make them SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

- Break them down into smaller steps: Large goals can be overwhelming. Break them down into smaller, manageable steps.

- Track your progress: Regularly review your progress towards your goals.

Conclusion – Taking Control of Your Finances

Creating a blank personal financial statement template is a significant step towards achieving financial stability and securing your future. By meticulously tracking your income, expenses, assets, and liabilities, you can gain a clear understanding of your financial situation and make informed decisions about your money. Remember that a financial statement is a dynamic tool that should be reviewed and updated regularly. Consistent tracking and analysis are key to maintaining control of your finances and working towards your long-term goals. Don't underestimate the power of a well-crafted financial statement – it's an investment in your future. Blank Personal Financial Statement Template – consistently utilizing this tool will undoubtedly lead to improved financial well-being. It's a continuous process of learning and adapting to changing circumstances. Continuous monitoring and adjustments are vital for maintaining a healthy financial trajectory.

0 Response to "Blank Personal Financial Statement Template"

Posting Komentar